The other side of the coin is China ’s attitude towards the overseas Chinese. As mentioned earlier, one of the narratives of Chinese civilization is that of Greater China, an idea which embraces the ‘lost territories’ of Hong Kong, Macao and Taiwan, the global Chinese diaspora and the mainland. The Middle Kingdom has always been regarded as the centre of the Chinese world, with Beijing at its heart and the disapora at its distant edges. All Chinese have held an essentially centripetal view of their world. The way that the diaspora has contributed to China ’s economic transformation is an indication of a continuing powerful sense of belonging. The rise of China will further enhance its appeal and prestige in the eyes of the diaspora and reinforce their sense of Chineseness. The Chinese government has sought, with considerable success, to encourage eminent overseas Chinese scholars to work and even settle in China. Meanwhile, as discussed earlier, Chinese migration is on the increase, notably to Africa, resulting in the creation of new, as well as enlarged, overseas Chinese communities. It is estimated that there are now at least half a million Chinese living in Africa, most of whom have arrived only very recently. There are over 7 million Chinese living in each of Indonesia, Malaysia and Thailand, over 1 million each in Myanmar and Russia, 1.3 million in Peru, 3.3 million in the United States, 700,000 in Australia and 400,000 in the UK; the approximate figure for the diaspora as a whole is 40 million, but this may well be a considerable underestimate.

How will this relationship between China and the diaspora develop? Will the mainland at some point consider allowing dual citizenship, which at the moment it does not? Is it conceivable that in the future there might be a Chinese Commonwealth which embraces the numerous overseas Chinese communities? Or, to put it another way, what forms might a Chinese civilization-state take in a modern world in which it is predominant? A commonwealth would no doubt be unacceptable to other nations as things stand, but in the event of a globally dominant China, the balance of power would be transformed and what is politically possible redefined. The impact of any such development would, of course, be felt most strongly in South-East Asia, where the overseas Chinese are, relatively speaking, both most powerful and most numerous.

ECONOMIC POWERHOUSE

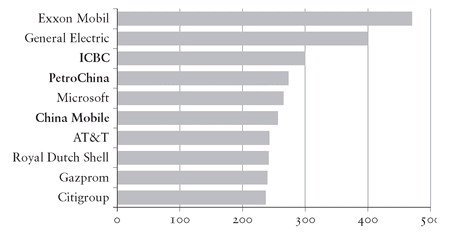

Chinese economic power will underpin its global hegemony. With the passing decades, as the Chinese economy becomes increasingly wealthy and sophisticated, so the nature of that power will no longer rest primarily on the country’s demographic clout. It is impossible to predict exactly what this might mean in terms of economic reach, but, given that China has a population around four times that of the United States, one might conjure with the idea that China ’s economy could be four times as large as that of the US. In mid 2007, before the credit crunch, with rapidly rising share prices on the Shanghai and Hong Kong stock exchanges, [1263] Chinese companies accounted for three of the ten largest companies in the world by market value (see Figure 46), and by the end of October that figure had risen to five out of ten. Citic Securities, the biggest publicly traded brokerage in China, trailed only Goldman Sachs, Morgan Stanley and Merrill Lynch in market value among securities firms, while Air China was the world’s biggest airline by market value, having overtaken Singapore Airlines and Lufthansa. [1264] Of course it may transpire, as happened with the value of Japanese companies in the asset bubble of the late eighties, that these figures prove to be considerably inflated, but nonetheless they are probably a rough indication of likely longer-term trends.

The potential volume of Chinese overseas investment, as China ’s capital account is steadily opened and the movement of capital liberalized, is huge, especially given the level of China ’s savings. In 2007 China had $4,800 billion in household and corporate savings, equivalent to about 160 per cent of its GDP. On the assumption that savings grow at 10 per cent per annum, China will have in the region of $17,700 billion in savings by 2020, by which time China should have an open capital account. If just 5 per cent of savings leaves the country in 2020, that would equal $885 billion in outward investments. If outflows reach 10 per cent of savings, $1,700 billion would go abroad. [1265] To provide some kind of perspective, in 2001 US invisible exports totalled $451.5 billion. At the time of writing, Chinese overseas investment is still, in historical terms, in its infancy, but it is growing extremely rapidly: China ’s overseas investment reached over $50 billion in 2008, with an annual average growth rate of 60 per cent between 2001 and 2006. [1266] A hint of what the future might hold was provided by the investments made by Chinese banks in Western financial institutions, which, in late 2007, found themselves seriously short of capital as a result of the credit squeeze which began in August of that year. By the end of 2007 Chinese financial institutions owned 20 per cent of Standard Bank, 9.9 per cent of Morgan Stanley, 10 per cent of Blackstone, and 2.6 per cent of Barclays. [1267] This, however, proved to be the high-water mark, as the Chinese government, increasingly aware of the depth of the American financial crisis, advised its banks to desist from becoming involved in rescue packages for beleaguered American and European banks.

Figure 46. World’s biggest companies by market capitalization, 28 August 2007, $bn (Chinese companies in bold).

There is plenty of evidence that China is steadily climbing the technological and scientific ladder. At present it is still a largely imitative rather than innovative economy, but the volume of serious scientific research is rising rapidly, as is expenditure on research and development. China is already the fifth leading nation in terms of its share of the world’s leading scientific publications and it is particularly strong in certain key areas like nanotechnol ogy. [1268] In 2006, according to the OECD, China overtook Japan to become the world’s second largest R & D investor after the US. [1269] With 6.5 million undergraduates and 0.5 million postgraduates studying science, engineering and medicine, China already has the world’s largest scientific workforce. [1270] In 2003 and 2005 it successfully carried out two manned space missions, [1271] while in 2007 it managed to destroy one of its own satellites with a ballistic missile, thereby announcing its intention of competing with the United States for military supremacy in space. [1272] In due course, it seems highly likely that China will emerge as a major global force in science and technology.

One of the more fundamental economic effects of the rise of China will be to transform and reshape the international financial system. By 2007, for the first time since 1918, when the dollar began to replace the pound as the world’s leading currency, it found itself with a new rival in the form of the euro. After 2002 the value of the dollar was steadily undermined by the effects of the United States ’ twin deficits (namely the balance-of-payments deficit and the government’s own deficit) combined with the slow long-term decline of the American economy discussed in Chapter 1. The decline in the dollar’s external value was precipitous: against the euro, by the end of 2007 it had depreciated by 40 per cent since its peak at the end of January 2002. [1273] It recovered significantly in late 2008, but this is likely to be a temporary respite. The financial crisis triggered in September 2008 suggests that the US is no longer economically strong enough to underwrite the present international economic system and sustain the dollar as the world’s premier reserve currency. The significance of the dollar’s decline, moreover, is not confined to the financial world but has much larger ramifications for Washington ’s place on the international stage. Flynt Leverett, a former senior National Security Council official under President George W. Bush, has argued that: ‘What has been said about the fall of the dollar is almost all couched in economic terms. But currency politics is very, very powerful and is part of what has made the US a hegemon for so long, like Britain before it.’ [1274] Similarly Kenneth Rogoff, former chief economist at the International Monetary Fund, wrote: ‘Americans will find global hegemony a lot more expensive if the dollar falls off its perch.’ [1275] The consequences of a falling dollar could be manifold: nations will prefer to hold a growing proportion of their reserves in currencies other than the dollar; countries that previously pegged their currency to the dollar, including China, will choose no longer to do so; the US will find that economic sanctions against countries like Iran and North Korea no longer carry the same threat because access to dollar financing has less significance for them; countries will no longer be so willing to hold their trade surpluses in US Treasury bonds; US military bases overseas will become markedly more expensive to finance; and the American public may be less prepared to accept the costs of expensive overseas military commitments. To put it another way, the US will find it more difficult and more expensive to be the global hegemon. The same kind of processes accompanied the decline of the pound, and Britain ’s position as an imperial power, between 1918 and 1967.

[1263] Hong Kong-listed shares surged after the Chinese government agreed in August 2007 that its citizens would be allowed to invest in the Hong Kong stock market. All five of China ’s biggest companies by market value in late 2007 had Hong Kong listings.

[1265] Jing Ulrich, ‘Insight: China Prepares for Overseas Investment’, Financial Times, 7 August 2007.

[1266] ‘ China ’s Overseas Investment Rises 60 % Annually’, 2 February 2007, posted on www.chinadaily.com.cn/bizchina.

[1267] ‘Morgan Stanley Taps China for $5bn’, Financial Times, 19 December 2007; Tony Jackson, ‘The Chinese Bank Plan is One to Watch’, Financial Times, 23 July 2007; Geoff Dyer and Sundeep Tucker, ‘In Search of Illumination: Chinese Companies Expand Overseas’, Financial Times, 3 December 2007.

[1268] Zhou Ping and Loet Leydesdorff, ‘The Emergence of China as a Leading Nation in Science’, Research Policy, 35 (2006), pp. 83-104.

[1269] James Wilsdon and James Keeley, ‘ China: The Next Science Superpower? The Atlas of Ideas: Mapping the New Geography of Science’ (London: Demos, 2007), p. 6.

[1270] Geoff Dyer, ‘The Dragon’s Lab — How China is Rising Through the Innovation Ranks’, Financial Times, 5 January 2007.

[1272] ‘China’s Missile Test Holds Signal for US’, International Herald Tribune, 20–21 January 2007; ‘China Uses Space Technology as Diplomatic Trump Card’, International Herald Tribune, 24 May 2007.

[1273] ‘It’s a Multi-Currency World We Live In’, Financial Times, 26 December 2007; Benn Steil, ‘A Rising Euro Threatens American Dominance’, Financial Times, 22 April 2008.