THE CHINESE MODEL

The transition from a command economy to a market economy, involving a major diminution in the role of the state, has understandably focused attention on the similarities between the Chinese economy and Western capitalist economies. It is becoming evident, however, that just as the Japanese and Korean economies have retained distinctive characteristics in comparison with the West, the same also applies to China. Given that the Chinese leadership consciously chose to follow the path of market reform, rather than having it imposed upon them by force majeure, as in the instance of Russia, this is not surprising. The key difference in China’s case concerns the role of the state. This should be seen as part of a much older Chinese tradition, as discussed in Chapter 4, where the state has always enjoyed a pivotal role in the economy and been universally accepted as the guardian and embodiment of society. The state in its various forms (central government, provincial government and local government) continues to play an extremely important role in the economy, notwithstanding the market reforms.

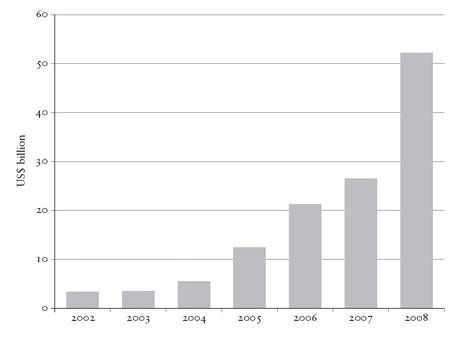

Figure 21. Growth of Chinese overseas investment.

Around the time of the Asian financial crisis in the late nineties, it appeared that China was on the verge of drastically contracting the role and number of its state-owned enterprises (many of which were highly inefficient and heavily subsidized), and following the well-worn path of privatization trodden by many other countries. In fact, a decade later, a rather different picture is emerging. Certainly, the number of state-owned enterprises has been severely reduced, from 120,000 in the mid nineties to 31,750 in 2004, a process which has been accompanied by major restructuring and pruning, with tens of thousands of jobs cut. [555] Rather than root-and-branch privatization, however, the government has sought to make the numerous state-owned enterprises that still remain as efficient and competitive as possible. As a result, the top 150 state-owned firms, far from being lame ducks, have instead become enormously profitable, the aggregate total of their profits reaching $150 billion in 2007. This has been part of a broader government strategy designed to create a cluster of internationally competitive Chinese companies, most of which are state-owned. Unlike the approach most countries have followed with regard to state-owned firms, which has seen them enjoying various degrees of protection, and often quasi-monopoly status, the Chinese government has instead exposed them to the fiercest competition, both amongst themselves and with foreign firms. They are also, unlike in many Western countries, allowed to raise large amounts of private capital. Of the twelve biggest initial public offerings on the Shanghai Stock Exchange in 2007, all were by state enterprises and together they accounted for 85 per cent of the total capital raised. Some of the largest have foreign stakeholders, which, despite tensions, has usually helped them to improve their performance. China ’s state-owned firms can best be described as hybrids in that they combine the characteristics of both private and state enterprises. [556] The leading state enterprises get help and assistance from their state benefactors but also have sufficient independence to be managed like private companies and can raise capital in the same way that they do. This hybrid approach also works in reverse: some of the largest privately owned companies, like the computer firm Lenovo and the telecommunications equipment maker Huawei, have been considerably helped by their close ties with the government, a relationship which to some extent mirrors the Japanese and Korean experience. Unlike in Japan or Korea, however, where privately owned firms overwhelmingly predominate, most of China ’s best-performing companies are to be found in the state sector. [557] The steel industry has been awash with private investment, but the industry leader and technologically most advanced producer is the state-owned Baosteel. Chinalco, also state-owned, has become one of the world’s largest producers of aluminium, and has designs on becoming a diversified metals multinational. Shanghai Electric is increasingly competing with Japan ’s Mitsubishi and Marubeni in bidding to build new coal-fired plants in Asia. China ’s two state-owned shipbuilding firms, China Shipbuilding Industry Corporation and China State Shipbuilding Corporation, are growing rapidly and starting to close the technological gap with their Korean and Japanese competitors. Chery, the state-owned car producer, with the fifth largest market share, has proved an extremely agile competitor and, given its limited resources, technologically ambitious and innovative. For the most part, it is these state-owned enterprises which are increasingly competing on the global stage with Western and Japanese companies.

The emergent Chinese model bears witness to a new kind of capitalism where the state is hyperactive and omnipresent in a range of different ways and forms: in providing assistance to private firms, in a galaxy of state-owned enterprises, in managing the process by which the renminbi slowly evolves towards fully convertible status and, above all, in being the architect of an economic strategy which has driven China’s economic transformation. China ’s success suggests that the Chinese model of the state is destined to exercise a powerful global influence, especially in the developing world, and thereby transform the terms of future economic debate. The collapse of the Anglo-American model in the wake of the credit crunch will make the Chinese model even more pertinent to many countries.

A MATTER OF SIZE

The combination of a huge population and an extremely high economic growth rate is providing the world with a completely new kind of experience: China is, quite literally, changing the world before our very eyes, taking it into completely uncharted territory. Such is the enormity of this shift and its impact on the world that one might talk of modern economic history being divided into BC and AC — Before China and After China — with 1978 being the great watershed. In this section I will concentrate on the economic implications of China ’s size.

When the United States began its take-off in 1870, its population was 40 million. By 1913 it had reached 98 million. Japan ’s population numbered 84 million at the start of its post-war growth in 1950 and 109 million by the end in 1973. In contrast, China ’s population was 963 million in 1978 when its take-off started in earnest: that is, twenty-four times that of the United States in 1870 and 11.5 times that of Japan in 1950. It is estimated that by the projected end of its take-off period in 2020, China ’s population will be at least 1.4 billion: that is, fourteen times that of the United States in 1913 and thirteen times that of Japan in 1973. If we broaden this picture, India had a population of 839 million in 1990 when it started its major take-off, nearly twenty-one times that of the United States in 1870 and ten times that of Japan in 1950. [558]

Total population is only one aspect of the effect of China ’s scale. The second is the size of its labour force. Although China ’s population presently accounts for 21 per cent of the world’s total, the proportion of the global labour force that it represents is, at 25 per cent, slightly higher. In 1978, when the great majority of its people worked on the land, China only had 118 million non-agricultural labourers. In 2002 that figure had already increased to 369 million, compared with a total of 455 million in the developed world. By 2020 it is estimated that there will be 533 million non-agricultural labourers in China, by which time it will exceed the equivalent figure for the whole of the developed world by no less than 100 million. In other words, China’s growth is leading to a huge increase in the number of people engaged in non-agricultural labour and, as a consequence, is providing a massive — and very rapid — addition to the world’s total non-agricultural labour force.

[555] Barry Naughton, The Chinese Economy: Transitions and Growth (Cambridge, Mass.: MIT Press, 2007), p. 313.

[556] Geoff Dyer and Richard McGregor, ‘ China ’s Champions: Why State Ownership is No Longer Proving a Dead Hand’, Financial Times, 16 March 2008.